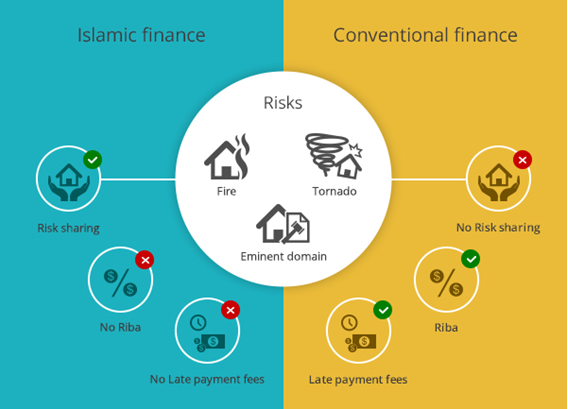

The main properties of Islamic finance include:

- The prohibition of taking or receiving interest;

- Capital must have a social and ethical purpose beyond pure, unfettered return;

- Investments in businesses addressing alcohol, gambling, drugs or anything that the Shariah considers unlawful are deemed undesirable and prohibited.

As per the international centre for education in Islamic finance prohibition on transactions involving maisir (speculation or gambling); and a prohibition on gharar, or uncertainty about the subject-matter and terms of contracts – this includes a prohibition on selling something that one doesn’t own. Because of the restriction on interest-earning investments, Islamic banks must obtain their earnings through profit-sharing investments or fee-based returns. When loans are given for business purposes, the lender, if he wants to form a legitimate gain under the Shari’ah, should participate within the risk. If a lender doesn’t participate within the risk, his receipt of any gain over the quantity loaned is classed as interest.

Islamic financial institutions even have the pliability to interact in leasing transactions, including leasing transactions with purchase options.

Traditionally an Islamic bank offers two sorts of services, as per a recent graduate of phd Islamic finance by coursework and research, and they are:

- Those for a fee or a set charge, like safe deposits, fund transfer, trade financing, property sales and purchases or handling investments; and

- Those who involve partnerships in investments and therefore the sharing of profits and losses.

PROPERTIES OF ISLAMIC FINANCE REGULATION:

Financial institutions seeking to supply shariah-compliant products typically have a shariah supervisory board (or at a minimum, a shariah counselor). The shariah board would review and approve financial practices and activities for compliance with Islamic principles. Such expertise raises the attractiveness of shariah-compliant financial intermediaries to investors considering SCF.

Shariah is hospitable interpretation and Islamic scholars aren’t in complete accordance regarding what constitutes SCF. Islamic finance laws and regulatory practices vary across countries. the dearth of concurrent viewpoints makes it difficult to standardize Islamic financing. Many observers view standardization of SCF regulations as important in increasing the marketability and acceptance of Islamic products.

International institutions are established to push international consistency in Islamic finance. for example, the Islamic Financial Services Boards (IFSB) puts forth standards for supervision and regulation. As another example, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), issues international standards on accounting, auditing, anD corporate governance.

Many leading Islamic financial centers round the world have adopted international SCF regulation standards. US federal banking regulators have provided some formal guidance about Islamic products. The Office of the Comptroller of the Currency (OCC) issued two directives concerning shariah-compliant mortgage products. In 1997, the OCC issued guidance about ijara (“lease”), a financial structure during which the financial intermediary purchases and subsequently leases an asset to a consumer for a fee. In 1999, the OCC recognized murabaha (“cost-plus”), under which the financial intermediary buys an asset for a customer with the understanding that the customer will buy the asset back for a better fee.

ALTERNATIVE PROPERTIES OF ISLAMIC FINANCE:

CONSUMER & BANK LOAN ALTERNATIVES:

The juristic-based understanding of forbidden riba/usury, and that Islamic finance must be “asset-based”, within the sense that one cannot collect or pay interest on rented money, joined does in conventional banking. Therefore, the easiest transactions to Islamize were secured lending operations, e.g., to finance the acquisition of assets, vehicles, business equipment, etc. Three main tools are utilized for this kind of retail financing:

Under Murabahah Transaction:

Buy-sell-back arrangements given the classical Arabic name: Murabahah. Under this transaction, the bank obtains a promise that its customer will purchase the property on credit at an agreed-upon mark-up (interest alternative), then proceeds to shop for the property and subsequently sell it to the customer. These are analogous to the Federal Reserve’s use of “matched-sale pur-chases.” looking on the jurisdiction and therefore the object of financing, this could or might not impose additional sales taxes, license fees, etc. In the U.K., a recent regulatory ruling allowed Islamic financiers (HSBC) to practice double-sale financing without being subject to double-duty taxation. In 1999, at the request of United Bank of Kuwait (UBK), which at the time offered an Islamic home financing program within the U.S. (called Manzil USA, the program was terminated shortly thereafter), the Office of the Comptroller of the Currency issued an interpretive letter declaring Murabaha financing to be “functionally adore or a natural outgrowth of secured property lending and inventory and equipment financing, activities that are a part of the business of banking”. The mark-up in Murabaha financing is benchmarked (i.e., made to track) conventional interest rates.

Lease-to-purchase or diminishing partnership arrangements:

under the Arabic names Ijara finance contract or Musharaka Mutanaqisa. A typical structure requires the bank to make a special purpose vehicle (SPV) to get and hold title to the financed property. The SPV then leases the property to the customer, who makes monthly payments that are part-rent and part-principal. Rents are calculated supported market interest rates, allowing monthly payments to follow a conventional amortization table. The juristic justification of this practice is that principal parts of monthly payments increase the customer’s ownership within the property, and permit him to pay less rent (on the part ostensibly owned by the bank through the SPV) over time, thus replicating a standard amortization table. Again, at the request of UBK, the Office of the Comptroller of the Currency examined the everyday structure of Islamic lease-to-own (Ijara) transactions, and reasoned as follows: “Today, banks structure leases in order that they’re resembling lending secured by personality … a lease that has the economic attributes of a loan is within the business of banking. Here it’s clear that UBK’s net lease is functionally corresponding to a financing transaction during which the Branch occupies the position of a secured lender…”

A new advantage to lease financing is that Islamic jurists allow the SPV to issue certificates securitizing the lease (ostensibly, the certificates represent ownership of the underlying asset, and thus allow their holders to gather rent). In recent years, this has given rise to a booming securitization industry in Islamic Finance, as we shall discuss within the context of bond-alternatives. Here within the U.S., both Federal National Mortgage Association and Freddie Mac have purchased and guaranteed Ijara-based mortgages, subject to their note requirements (which required overcoming some legal and juristic hurdles). Those Islamic mortgage-backed securities are currently being marketed as fixed-income investment alternatives for Muslims.

Role of GCC:

Recently, banks in Gulf Cooperation Council (GCC) countries are offering consumer finance through a three-party contract known by the Arabic name Tawarruq (literally: monetization of some commodity). this can be a practice that Islamic banks have used with more sophisticated business clients for variety of years, but only recently introduced for consumer financing. as an example, a customer wants to borrow $1000 using an Islamic Juristic-compliant mechanism. GCC Islamic jurists, counting on an opinion within the Hanbali school of jurisprudence, which is dominant therein region, allow the bank to shop for $1,000- worth of commodities (e.g., wheat), and sell them to the customer on credit at a mark-up (equal to the rate they’d have charged on a loan, perhaps plus compensation for the transaction costs related to multiple sales). The customer may then spin and sell the commodity to a 3rd party (oftentimes the identical party that sold it to the bank), collecting the required cash immediately, with a deferred debt capable principal plus interest. In 2004, a minimum of one other bank in a very GCC country announced a brand new Tawarruq facility. Since this sort of financing can easily replace lending for any purpose (consumer loans, unsecured loans, etc.), it’s allowed variety of conventional banks to announce that they’ll “Islamize” all of their operations. the foremost significant such announcement was that made by Saudi Arabia’s National Commercial Bank, stating that it planned to Islamize all of its lending practices by 2005.